Traditional debt collection systems often segment customers only by delinquency level, number of overdue days, or credit score. But within the same delinquency level, borrower behavior can differ substantially: some people simply forget a payment, some face temporary cash-flow difficulties, some avoid contact because of anxiety, and some systematically test the boundaries of tolerance.

In this case study, I explored not just delinquency as a fact, but behavior within the same delinquency status. The core idea is simple: the same delinquency does not mean the same borrower. If behavioral profiles differ, then the interaction strategy should differ as well.

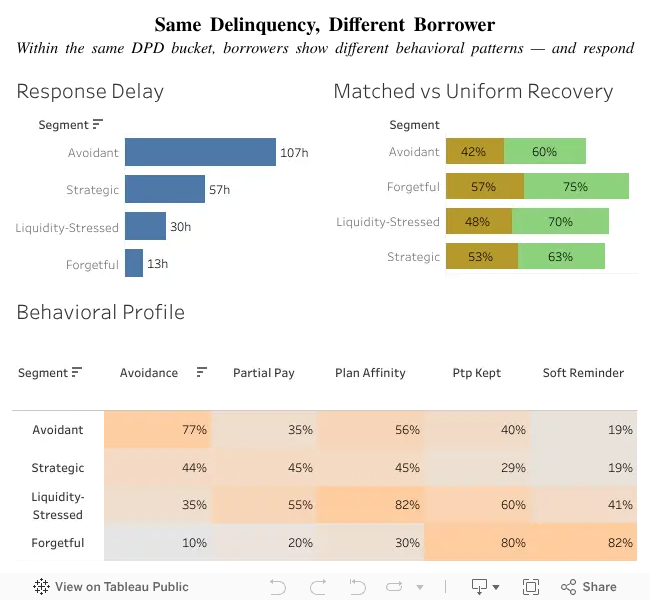

What the chart showed

Even within the same delinquency level, borrower responses turned out to be far from identical. For some customers, the time from reminder to action was only 13 hours, while for contact-avoidant profiles the response delay reached 107 hours. This means that delinquency level alone does not explain how a person behaves under financial pressure.

The visualization also shows that a strategy matched to a behavioral profile appears stronger than a one-size-fits-all approach. For some, a simple reminder works; for others, a flexible payment schedule is more effective; and for specific segments, faster escalation is more appropriate.

Response speed

Time from reminder to action turned out to be one of the strongest behavioral signals. It reflects not just slowness, but a person’s way of interacting with financial stress.

Matched approach

Within the model, a tailored debt collection approach delivers a better expected outcome than the same workflow for everyone. The advantage comes not from being stricter, but from more accurately targeting the cause of delay.

Behavioral profile

Within the same delinquency level, different patterns become visible: avoidance, cooperativeness, forgetfulness, and strategic delay. These patterns — not just overdue days — should shape the interaction strategy.

Four behavioral segments

Instead of treating all borrowers as one undifferentiated group, I broke the same delinquency level into four behavioral types. This makes it possible to see the psychological mechanism behind financial behavior, not just the debt status.

The forgetful

Usually pay on time, but occasionally miss a due date or react with a small delay. For them, a gentle reminder and a simple payment path are usually enough.

Temporary cash-flow stress

They are not intentionally avoiding payment, but are experiencing a temporary shortage of funds. Flexible scheduling, smaller payment parts, and due-date shifts work better for this profile.

Those who avoid action

They postpone contact and decisions even when the situation can still be stabilized. Calm, low-pressure communication with a clear and simple path to action works better here.

Strategic delayers

They regularly test boundaries and use payment delay as part of their own strategy. They require a faster move toward a stricter scenario and less leniency.

Operational logic

- Customers who respond quickly and usually keep their promise to pay are best routed into a soft digital workflow with a simple payment link.

- Customers facing temporary cash-flow stress should be offered schedule changes, smaller payment parts, or postponement.

- For those who avoid contact and delay their response, more aggressive communication can worsen the outcome; a calm, structured, low-pressure scenario is likely to be more effective.

- For customers who systematically delay payment, the route should be stricter and move to escalation faster.

Key takeaway

The same delinquency can hide different behavioral mechanisms, which means that the same interaction strategy for all customers is logically weak.

The best debt collection systems are not necessarily tougher. They are more accurately matched to the type of behavior. Pressuring a person who avoids contact only intensifies resistance. Giving an overly soft regime to a strategic delayer reinforces a pattern that is unfavorable for the company.

The same delinquency does not mean the same borrower.

Practical relevance

Debt collection can be built more precisely if customers are segmented not only by delinquency or score, but also by behavior.

The practical value of this approach lies in more accurate routing, fewer misfired actions, and a better balance between debt recovery and customer experience.

Not all borrowers should be reduced to the same type. A person facing temporary difficulty and a person who systematically delays payment are not the same situation.

A more behaviorally sensitive system can be both more effective for the company and less damaging to the customer experience.

This case shows how a synthetic but realistic research environment can be built in which segmentation relies not only on risk, but also on behavioral signals.

The visual layer was built in Tableau, while the data structure and feature logic were developed in Python and VS Code.

Methodology and technical details

This is a synthetic portfolio case built on contemporary debt collection practice, behavioral segmentation, affordability assessment logic, and principles for working with vulnerable customers.

Open the technical section

Case type

A synthetic portfolio case built on contemporary debt collection practice, behavioral segmentation, and regulatory approaches to vulnerable customers.

Data structure

- One delinquency level: 16 to 30 days overdue.

- Base features: days overdue, debt amount, number of missed payments, customer tenure, history of previous delinquencies.

- Behavioral features: response speed to reminders, kept promise-to-pay, frequency of partial payments, contact avoidance, sensitivity to flexible repayment schedules.

- Additional affordability layer: income instability, end-of-month financial pressure, and a proxy cash-reserve indicator.

Segmentation approach

The goal of the segmentation here is not to predict default as such, but to show that the same delinquency status can hide different behavioral mechanisms and may require different interaction scenarios.

Tools

- Python

- VS Code

- Tableau

Why the data is synthetic

Public datasets that simultaneously include delinquency status, response to reminders, communication channels, outcomes of different engagement strategies, and behavioral signals are almost unavailable because of privacy and regulatory constraints.

Sources of logic

- McKinsey: behavioral segmentation and innovative approaches in collections.

- FCA: approach to fair treatment of vulnerable customers.

- Contemporary affordability assessment practices based on cash-flow signals and temporary financial stress indicators.